FR

FR DE

DE EN

EN En vedette

En vedette

What is AML transaction supervision?

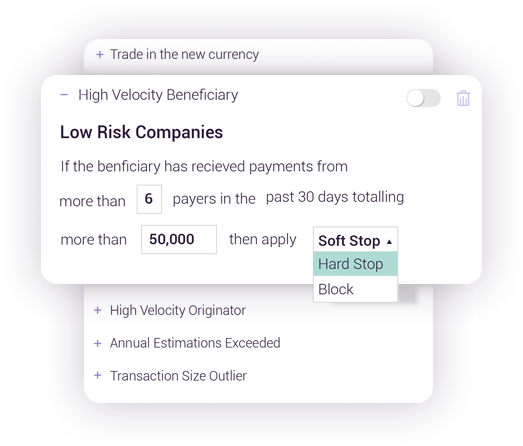

Anti-Money Laundering (AML) transaction monitoring software allows banks and other financial institutions to monitor customer transactions for risk on a daily or real-time basis. By combining this information with analysis of historical customer information and account profile, the software can provide financial institutions with a « big picture » analysis of customer profile, risk levels and expected future activities, and can also generate reports and create alerts in case of suspicious activity. Monitored transactions may include cash deposits and withdrawals and wire transfers.

AML transaction monitoring solutions can also include sanctions screening, blacklist screening and customer profiling functions. The analysis is obtained primarily for the purpose of satisfying various anti- money laundering (AML) and anti-terrorist financing (FT) requirements, filing suspicious activity reports (DAS) and completing other reporting obligations. Some regulators around the world make transaction monitoring a specific regulatory requirement, in New York State Part 504 does so as does the 4th Money Laundering Directive in Europe for high-risk relationships.

laundering (AML) and anti-terrorist financing (FT) requirements, filing suspicious activity reports (DAS) and completing other reporting obligations. Some regulators around the world make transaction monitoring a specific regulatory requirement, in New York State Part 504 does so as does the 4th Money Laundering Directive in Europe for high-risk relationships.

How does transaction monitoring work?

- Identify suspicious behavior – at the end customer level

- Increase automation – minimize unnecessary alerts by tailoring scenarios to customer or transaction risks and focusing on regulatory priorities.

- Increase efficiency over time – establish the rules without the help of a technician.

- Giving confidence to regulators and banking partners – a ‘proven’ system with a clear audit trail for monitoring and investigations

- Fast, easy and secure implementation – easy to implement with REST API or batch file upload

Transaction oversight and risk-based approach

Generally speaking, a risk-based approach requires financial institutions to apply intensive measures (such as increased due diligence ) to manage risk for customers or scenarios deemed riskier, while for customers or low-risk scenarios. risk, and where there is no suspicion of money laundering or terrorist financing, simplified measures may be authorised.

To apply a risk-based approach, countries and institutions should take appropriate steps to identify and assess money laundering and terrorist financing risks for different market segments, intermediaries and products on an ongoing basis. In line with the concept of risk-based approach, it is recognized that the nature and extent of AML/CFT controls will depend on a number of factors. The FATF, the global financial body that sets standards for AML/CFT procedures, recognizes the following factors as determinants of the appropriate scope of AML/CFT controls:

- The nature, scale and complexity of a financial institution’s business.

- The diversity of a financial institution’s business, including geographic diversity.

- The financial institution’s customer, product and business profile.

- The distribution channels used. The volume and size of transactions.

- The degree of risk associated with each line of business of the financial institution.

- The extent to which the financial institution deals directly with the customer or deals through intermediaries, third parties, correspondents or access.

Our AML transaction monitoring solutions help you monitor people, entities and transactions to quickly and effectively detect suspicious activity.

To know more :

[siblings post_type= »knowledgebase »]

Publié initialement 31 octobre 2019, mis à jour 31 mars 2023

Contenus associés

En vedette

Avertissement : Ce document est destiné à des informations générales uniquement. Les informations présentées ne constituent pas un avis juridique. ComplyAdvantage n'accepte aucune responsabilité pour les informations contenues dans le présent document et décline et exclut toute responsabilité quant au contenu ou aux mesures prises sur la base de ces informations.

Copyright © 2023 IVXS UK Limited (commercialisant sous le nom de ComplyAdvantage)