EN

ENScreening for Cyber Crime Money Laundering

Ensure your organization is well protected with our anti-money laundering screening tool.

In a data-driven financial landscape, cyber crime has emerged as a significant concern for regulators and institutions alike, with criminals exploiting computer systems and online financial services to perpetrate money laundering, fraud and other crimes. In 2015, cyber crime cost the global economy around $3 trillion, with that figure expected to rise to $6 trillion in 2021. The cost of cyber crime money laundering is expected to grow by around 15% annually over the next 5 years, reaching around $10.5 trillion in 2025.

The threat posed by cyber crime money laundering methodologies has been exacerbated by the Covid-19 pandemic. With an increase in online financial activity and changes in customer behavior, criminals have been able to target vulnerable individuals and institutions more easily and take advantage of regulatory blind spots.

Given the threat, and the potential for significant penalties, banks, financial institutions and other obligated entities should ensure that they understand the compliance risks they face and be prepared to deploy a suitable cyber crime money laundering response.

Although there is no universally codified definition, cyber crime is generally understood to be any crime that is perpetrated online or that involves the use of a computer. Cyber crimes may be separated into two categories of crime:

With the emergence and growing ubiquity of online commercial and financial services (especially during the Covid-19 crisis), criminals have had greater opportunities to derive profits from online fraud and theft and, with that, a greater need to conceal the source of their illegal funds.

Computers and computer systems offer money launderers a degree of anonymity and the opportunity to move illegal funds quickly between accounts while avoiding the customer due diligence and transaction monitoring checks that conventional AML/CFT systems would normally impose.

Cyber crimes involve a wide variety of approaches and methodologies. Specific examples include:

Cybercriminals may use the approaches set out above to steal financial data, card payment data, user identities, or to perform extortion (using the threat of more severe cyber-attacks).

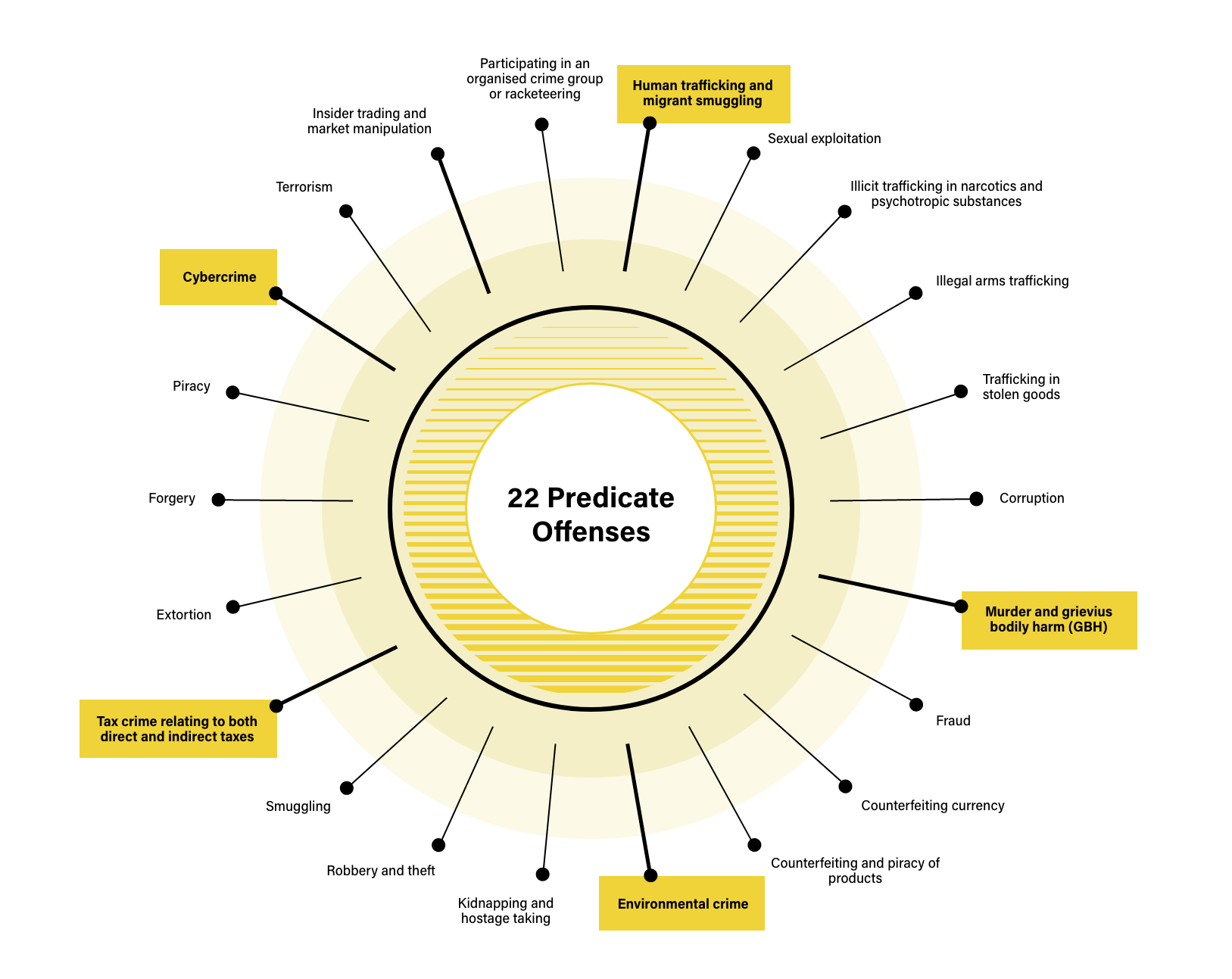

Predicate offence: Cyber crime money laundering is considered a predicate offence in the sense that it generates illegal proceeds that need to be disguised by laundering before they can be entered into the legitimate financial system. The European Union’s 6th Ant-Money Laundering Directive (6AMLD) codifies this by including cyber crime in its list of 22 money laundering predicate offences, joining existing predicate offences like human trafficking, drug trafficking, counterfeiting, and theft.

In adding cyber crime money laundering to the 6AMLD list of predicate offences, the EU has introduced a new compliance obligation: under 6AMLD rules, firms must screen their customers and transactions for evidence of cyber crime money laundering activities – a process which involves performing risk assessments and examining transactional behavior.

Cyber crimes often exhibit ‘red flag’ characteristics that can aid firms in detecting and preventing money laundering and in enhancing their compliance performance. In response to the global pandemic, the Financial Crimes Enforcement Network (FINCEN) recently released a series of advisories calling on financial institutions to be particularly vigilant for cyber crime Covid-19 related attempts to launder money. With those advisories in mind, red flags that indicate cyber crime money laundering include:

Under Financial Action Task Force (FATF) recommendations, banks, financial institutions and other obligated entities must put risk-based AML/CFT programs in place to deal with the AML/CFT threats that they face from cyber crime money laundering. In practice this means that firms must conduct risk assessments of their customers and deploy a proportionate AML response. In the context of cyber crime, this means that firms must work to identify their customers and to monitor their transactional behavior on an ongoing basis with the following AML/CFT measures and controls:

Ensure your organization is well protected with our anti-money laundering screening tool.

Originally published 24 February 2021, updated 29 November 2022

Disclaimer: This is for general information only. The information presented does not constitute legal advice. ComplyAdvantage accepts no responsibility for any information contained herein and disclaims and excludes any liability in respect of the contents or for action taken based on this information.

Copyright © 2023 IVXS UK Limited (trading as ComplyAdvantage).