Enhanced due diligence (EDD) involves determining, based on a risk-based approach, to investigate particular clients more thoroughly – requiring significantly more evidence and detailed information about reputation and history to be collected.

EDD is especially relevant for high-risk or high-net-worth customers or those who conduct large or unusual transactions, which pose more significant risks.

Every year around $2tn in illicit cash flows through the global financial system despite governments, regulators, and financial institutions trying to maintain financial stability through new legislation, enforcement actions, and improved collaboration.

In addition, FATF’s Recommendation 19 states that EDD measures should be carried out on “business relationships and transactions with natural and legal persons, and financial institutions, from countries for which this is called for by the FATF.” Institutions should implement KYC/AML and all CDD measures for new business relationships, occasional transactions if there is a suspicion of money laundering or terrorism financing, or unreliable documentation. Monitoring should be ongoing rather than a one-off obligation.

EDD practical steps suggested by the FATF include:

Accessing additional identifying information from a wider variety of sources

Carrying out additional searches

Verifying the source of funds involved to ensure they are not proceeds from crime

Gaining additional information from the customer about the purpose and nature of business relationships

Commissioning an intelligence report on the customer or beneficial owner

How Does the Enhanced Due Diligence Process Work?

Following FATF guidance, companies should implement risk-based EDD measures that reflect the specific AML/CFT risk that individual customers present. These should include:

Applying closer scrutiny to the nature of the business relationship or purpose of a transaction

Implementing ongoing monitoring procedures

For many of the persons and entities identified, enhanced due diligence will be a standard part of their relationship with a firm.

An alert could also trigger EDD in a transaction monitoring system if it’s flagged for further investigation. Additional information – either from a relationship manager or the client – may be needed, and firms should make internal and external inquiries to learn more about the customer and the transaction.

Identify risks before they become threats

Ensure your firm has effective EDD measures in place. Screen against the world’s only dynamic global database of Sanctions and Watchlists, PEPs, and Adverse Media, in consolidated, structured profiles.

Firms should be able to comply quickly and efficiently with requests for records from regulators and enable authorities to reconstruct individual transactions, including details of the amounts of money and types of currency involved.

Where CDD measures create suspicion or reasonable grounds to suggest that a customer is involved in criminal activity, companies must report that information promptly to their jurisdiction’s financial intelligence unit (FIU) via a suspicious activity report (SAR).

Regulatory requirements will differ in local jurisdictions, so firms should check their operating areas.

While adverse media is not a regulatory requirement for enhanced due diligence, it can be a powerful tool. It may reveal involvement with money laundering, financial fraud, drug trafficking, human trafficking, financial threats, organized crime, terrorism, or other criminal activity.

In Europe, Article 18 of 4AMLD states that businesses located in a country listed as a high-risk third country require EDD. And any politically exposed persons (PEPs), their close associates, or family members must also be thoroughly examined.

It is also important in all jurisdictions to keep updated on constantly evolving AML sanctions. Regular screening is needed to ensure your customers are not on any watch lists. Industries at increased risk of money laundering, such as gambling, also often have KYC enhanced due diligence requirements in many parts of the world.

In the US, FinCEN guidance warns that the scope of due diligence measures will vary on a case-by-case basis.

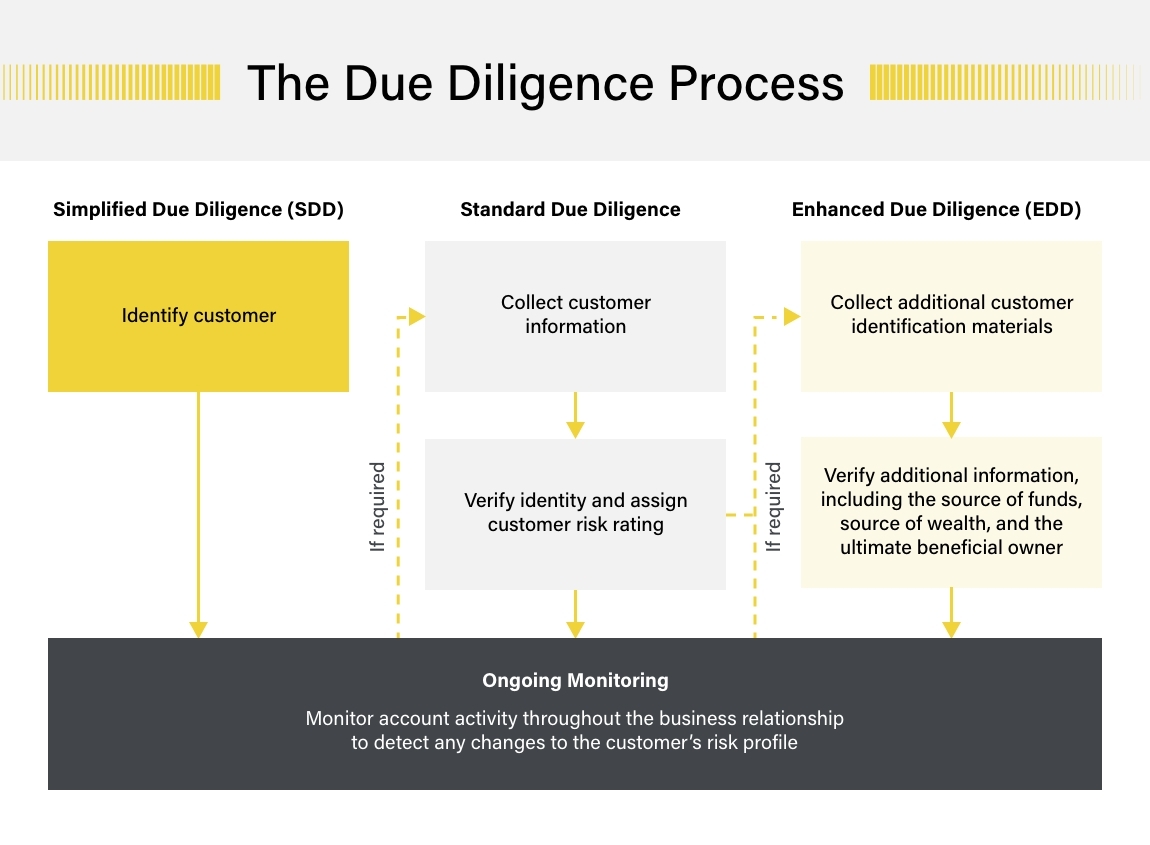

Customer Due Diligence vs. Enhanced Due Diligence

There are three levels of due diligence – simplified, CDD, and EDD.

There are several characteristics that distinguish EDD from regular CDD policies:

Rigorous and robust: Enhanced due diligence policies require significantly more evidence and detailed information than essential regulatory obligations of customer identification, establishing ultimate beneficial ownership, and business relationship nature and purpose

Reasonable assurance: EDD requirements should provide “reasonable assurance” when calculating a KYC risk rating. Responsible investigators should complete all necessary research steps and exercise professional skill and judgement in making decisions

Detailed documentation: The EDD process must be documented in detail, with scrutiny on how data is captured and validating the reliability of information sources

PEPs: Special attention should be paid to PEPs, who are in positions that can be potentially abused for money laundering.

Effective enhanced due diligence measures are built on a combination of technology and expertise.

As risk profiles and criminal behaviours evolve, firms must be as flexible and innovative with their approach to EDD as with other aspects of their AML/CFT policy. Technology provides valuable tools to facilitate EDD processes, but human vigilance is vital to spot and address new threats.

EDD also requires “reasonable assurance” when calculating aKYC risk rating. This means that the professionals responsible for making a decision must have completed all the necessary research steps and exercised professional skill and care in reaching their judgement.

Disclaimer: This is for general information only. The information presented does not constitute legal advice. ComplyAdvantage accepts no responsibility for any information contained herein and disclaims and excludes any liability in respect of the contents or for action taken based on this information.

EN

EN DE

DE